Financials 101: Part 2 of 3

B-b-b-budgeting, baby!

TIPS & TRICKSHUSTLING

Whether you work as independent artist or not, you should probably have a budget to track your finances. Budgets are helpful tools to track your income (the money you earn) and your expenses (the money you spend).

This introductory post will cover two types of budgets: budgets you build for yourself, and budgets you build for projects (for the purposes of getting grants or submitting project proposals)

Your Budget

Why budget? A budget helps you divide your income between: what you need, what you want, your savings, and debt repayment in a way that can help keep your focus on so your expenses don't go totally off the rails.

A budget is a tool to plan where your dollars are going. It's only as succesful as you are with referencing it before you spend a penny. Say you want to buy a new computer in 3 months. Let's say that computer is $1,155. To have that $1,155 in 3 months, you should be planning to set aside $385 a month (total amount divided by number of months).

Budgets help you make a plan by looking at all your income and dividing it accordingly to get what you need (rent, groceries, gas), what you want (new computer, fun night out), savings (what you need later or in case of emergencies), and debt repayment (credit cards, loans).

To build a budget, it's helpful to know your spending habits. Assuming you have a bank account where you stash your income, most banks with online banking features can generate charts that breakdown your expenses.

There are also cool apps like Mint that you can connect to your checking account, credit cards, PayPal, etc. to see your cash flow trends.

Having that data is great for building your budget. So. To build your budget, let's try and break down what you're hoping to do in a month: pay your rent, utilities, car insurance, buy groceries, go out to eat, maybe buy some new clothes, buy supplies, contribute to your Roth IRA because you hope to retire...yada yada

Some of these numbers are usually consistent (rent, utilities, retirement, car payments)

Some of these numbers fluxuate, but with your banking app or something like Mint, you can see, on average, how much you spend in large categories on a monthly basis to create a budget (weekly avg. on groceries, gas, shopping)

Some of these numbers can act as goals. Say you hope to stash more into your savings this month. Your budget can predict how much you can, and then when your income comes in, you can see how much you really can save.

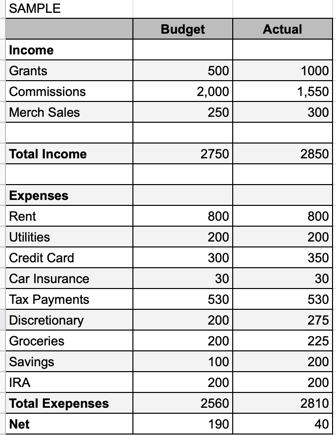

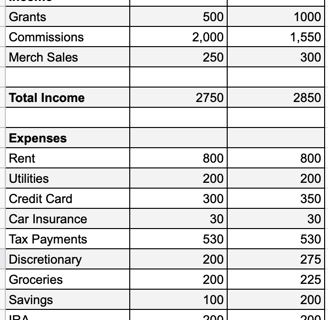

Consider the sample above. You can pop into Google Sheets or Excel, or a fancy budgeting app, and start setting up your core sources of income and expenses. You want to recreate this for each month to get a snapshot of where you're money's coming from and going and where you'd like it to go.

It's essential to update your budget on a monthly basis to see where you're at with your goals.

When you're first setting up your budget, all these numbers can feel sort of arbitrary, but start with the core payments you have to make every month to survive like rent and bills and go from there. For setting goals, I refer you to Nerd Walletbecause they have all kinds of helpful information and tools that can help you set goals for your budget based on your monthly income (Nerd Wallet is also a great source for shopping out a new credit card, but that's a conversation for another time).

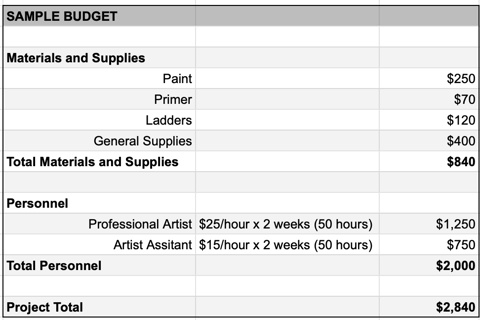

Project Budgets

If you're submitting proposals for grants or murals or you do other types of freelance work, it's very helpful to know how much it costs for you to your job, which is produce artwork in this case.

Project budgets, at the core, consist of the costs of materials & labor. Some grant applications include budget templates for specific applications, you see that a lot from government funded entities (i.e. Georgia Council for the Arts). Project budgets help funders see what they're getting for their dollar.

Project budgets can also just be helpful references for you if you want to pay yourself honestly for your work or if you're investing in a project all your own like self-publishing a book. These budgets can look really simple or more involved depending on the size and length of the project.

Cost of materials is pretty easy. How much does it cost for your craft? Amount of paint gallons needed to cover a 700 square foot wall, brushes, ladder, etc. Even if you're working soley digital, consider the total cost of your computer or tablet. If you're making payments on technology, you could factor that into part of your technology material cost when building a project budget.

Labor is usually the trickiest part for most folks, because, yeah, how do you charge for your time and effort? Well, here's the solution to this mysertious trick: pay yourself a living wage! How much you need to live usually depends on where you live. And additions to your living wage rate would be your level of experience. You have to promote yourself overtime as your skills improve, as you build a more impressive portfolio. Just because you're working independently, doesn't mean you shouldn't treat yourself like an employee. But be realistic. If you're just getting started, maybe start with the base living wage with where you live and then consider annual raises (3-4%) if you're consistenly getting projects and improving your craft.

With labor, you also have to be realistic about how long you'll work, and how long it takes you to complete a project. Say you're working 5 hour days for 10 days, that's the kind of info that will help your project budget (i.e. Artist Labor: $25/hour x 2 weeks (50 hours) = $1,250)

For more details on building budgets for your art, check out this Fractured Atlas article for a deeper dive.

That's all we have for now, folks. Hopefully this lays a nice foundation to help you start thinking about budgets and feeling more empowered. Numbers, math, and money can be stressful, but these tools are here to help you and they're not all too scary once you dig in! Come back for Part 3 of Financials 101 where we talk about Banking & Credit.

About

The Show List

Grants & Residences

Submit a resource

Keep It Weird © 2024

Keep It Weird. Keep DIY Alive.

If you value the info provided here for free, please consider leaving a tip!